Introduction

The escalating 2026 Middle East conflict provides a critical lens to examine the indispensability of marine insurance. While exorbitant war risk premiums and sudden coverage cancellations appear commercially disadvantageous, these mechanisms provide an overriding advantage: shielding stakeholders from catastrophic liabilities and satisfying strict trade finance covenants.

This article proceeds by defining the foundational framework of marine insurance and the Institute Cargo Clauses. It subsequently analyses standard exclusions, examines the immediate financial and banking implications of the Strait of Hormuz crisis, and concludes by unpacking the macro-jurisprudential and micro-contractual ramifications for the global trade and legal sectors.

Defining Marine Insurance

Marine insurance is a contractual arrangement providing indemnity against loss of or damage to ships, cargo, terminals, and associated transport assets engaged in the movement of goods across jurisdictions. In its absence, the transnational carriage of high-value goods would be commercially unviable, as no single party could reasonably assume the magnitude of potential maritime risks.

The key parties/terms are:

- The Insured: This includes the Shipowner (who insures the physical ship via “Hull and Machinery” insurance), the Charterer (who rents the ship), or the Cargo Owner (the buyer or seller of the goods).

- The Insurer: These are underwriting syndicates (like Lloyd’s of London) who cover the physical ships and cargo, and P&I Clubs (Protection and Indemnity mutuals) which cover third-party liabilities like oil spills or crew injuries.

- Who Pays the Premium? The shipowner pays the baseline hull and P&I premiums. For the goods inside, the premium is paid by either the exporter or the importer, depending on their agreed commercial contracts (Incoterms). However, during geopolitical crises, if a ship is ordered into a war zone, the charterer (the one renting the ship) is usually legally required to absorb any massive spikes in war risk premiums.

The Core Framework: Institute Cargo Clauses

The vast majority of global marine cargo policies are governed by the Institute Cargo Clauses (ICC), which dictate the scope of coverage in three main tiers:

- ICC (A) – All Risks: The broadest level of coverage. It protects against all risks of loss or damage to the cargo, minus a specific set of standard exclusions.

- ICC (B) – Named Perils: A moderate tier. It only kicks in for specific “named” disasters, such as fire, explosion, sinking, overturning, collisions, or water damage from the sea entering the vessel.

- ICC (C) – Basic Named Perils: The most restrictive tier. It covers major catastrophes like a sunken ship or a fire, but usually excludes things like goods washing overboard.

The Standard Exclusions

Even the broadest “All Risks” ICC (A) policies have strict limitations. If a loss is caused by an excluded event, the insurer will deny the claim. Common exclusions include:

- Inadequate Packing: If fragile electronics are shipped in flimsy cardboard without shock absorption and break in rough seas, the claim is denied.

- Inherent Vice: This applies to goods that naturally degrade. If a shipment of fresh fruit rots during a standard, on-time voyage due to its natural lifespan, the insurer will not pay.

- Willful Misconduct: Any intentional damage or sabotage by the insured party is strictly excluded.

- War Exclusion: In standard marine policies, the War Exclusion Clause strictly denies coverage for damage caused by war, civil war, revolution, capture, seizure, or derelict weapons of war (like floating mines or stray drones).

To legally and safely sail through conflict zones, shipowners must “buy back” this coverage by purchasing specific Institute War Clauses for an Additional War Risk Premium (AWRP). Insurers rely on the Joint War Committee (JWC), which maintains a real-time list of high-risk areas.

When a region turns hostile, insurers utilise a Notice of Cancellation. With just 48 to 72 hours’ notice, insurers can strip a vessel of its baseline war coverage. Shipowners are then forced to buy new, transit-specific coverage that usually only lasts for 7 days.

The Current Scenario: The 2026 Middle East Crisis

The ongoing 2026 conflict involving the US, Israel, and Iran perfectly illustrates how geopolitical risk dictates global trade. The Strait of Hormuz, which handles roughly 20% of the world’s global oil supply, is entirely designated as a high-risk zone.

When the conflict escalated in early 2026, underwriters triggered their Notices of Cancellation. Today, premiums—which are calculated as a percentage of a ship’s total Hull and Machinery value—have skyrocketed for a standard 7-day transit:

- Pre-Conflict Baseline (Early Feb 2026): 0.15% to 0.25%

- “Plain Vanilla” Vessels (No perceived conflict ties): 0.8% to 1.5%

- Standard Strait of Hormuz Transits: ~2.5%

- High-Risk / “Missile Magnet” Vessels (US, UK, or Israeli nexus): 5% to 7.5%, with some underwriters quoting “go-away pricing” of 10%.

The Financial Reality: For a Very Large Crude Carrier (VLCC) valued at $138 million, a 7.5% premium means the charterer must pay over $10 million in insurance just for a single 7-day voyage through the Strait.

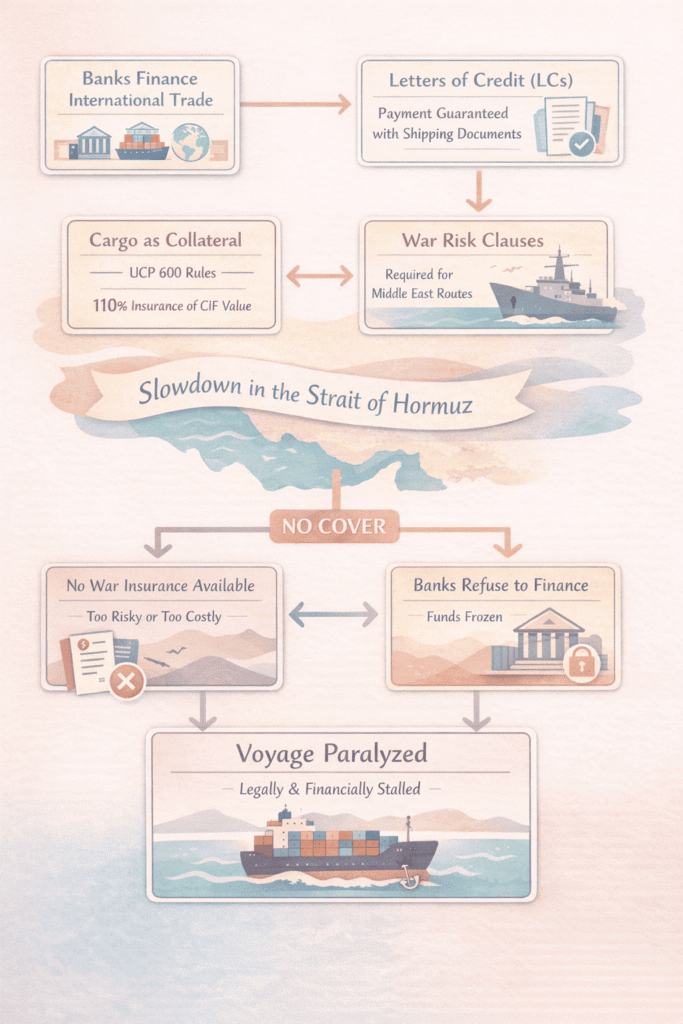

The Invisible Mechanism: Current Involvement of Banks

Banks heavily finance international trade through instruments like Letters of Credit (LCs), guaranteeing a seller gets paid once compliant shipping documents are presented. To a bank, the cargo is the collateral.

Under international banking rules (UCP 600), banks mandate strict insurance (usually 110% of the cargo’s CIF value). If a ship is passing through the Middle East, banks explicitly require the inclusion of War Risk clauses.

The current slowdown in the Strait of Hormuz is as much a financial blockade as a military one. If underwriters refuse to issue war cover or if it becomes too expensive for the charterer to buy banks will refuse to finance the cargo or release funds. In absence of bank backing, the voyage is legally and financially paralysed.

Lawsplained

The Macro Level: Systemic Shockwaves and Global Jurisprudence

At the highest levels of international law, a sudden conflict and subsequent insurance blockade redefine the legal landscape for years to come.

- The Boom in International Arbitration: Major shipping and insurance disputes are rarely settled in local courts; they are fought in international arbitration hubs like London (LMAA), Singapore (SCMA), and New York (SMA). The sudden cancellation of war risk covers and the rerouting of hundreds of vessels trigger a massive surge in cross-border arbitration over billions of dollars in delayed or ruined cargo.

- Redefining “Force Majeure” and Frustration: Legal disputes centre on whether designation of a “High-Risk Area” by the Joint War Committee constitutes a force majeure event or frustration of contract. Judicial and arbitral determinations in this regard establish binding precedents with long-term contractual implications.

- Sanctions and Regulatory Minefields: The legal sector must navigate a rapidly shifting web of international sanctions. When a conflict involves the US, Iran, and allied nations, global law firms must advise insurers and banks on whether paying a claim or financing a specific vessel violates new Office of Foreign Assets Control (OFAC) or UK/EU sanctions, risking severe criminal penalties.

- Rewriting Standard Contracts: Macro-level legal organizations, such as BIMCO (the Baltic and International Maritime Council), are forced back to the drawing board to draft new, standardized war clauses. They must update the legal definitions of “war” to include contemporary risks, cyber interference and autonomous attacks, to ensure contractual clarity and enforceability.

The Micro Level: Day-to-Day Legal Triage

On the ground, boutique maritime firms, banking lawyers, and corporate in-house counsel face a chaotic period of legal triage, putting out daily operational fires.

- Charterparty Disputes: A “Charterparty” is the lease agreement between a shipowner and a charterer. When underwriters issue a 72-hour Notice of Cancellation for war coverage, micro-level disputes explode. Lawyers are hired to aggressively litigate standard clauses (like CONWARTIME) particularly in relation to voyage orders and liability for increased premiums.

- Trade Finance & UCP 600 Constraints: Banking lawyers are heavily engaged when exporters try to cash out. Under the Uniform Customs and Practice for Documentary Credits (UCP 600), banks demand perfect paperwork. If an exporter’s insurance certificate shows a war exclusion because the premium was too high, banking lawyers immediately advise the bank to reject the Letter of Credit, freezing the exporter’s funds.

- The In-House Counsel: For the lawyers working directly inside logistics companies, it becomes a 24/7 job of damage control. They must rapidly draft and issue “Notices of Route Deviation” to clients, legally justify the imposition of sudden “War Risk Surcharges” on invoices, and defend against breach-of-contract claims from buyers furious that their perishable goods have been rotting on a delayed ship for three weeks.

- Billable Hours and Resource Strain: For private practice maritime and insurance lawyers, a geopolitical shipping crisis leads to a massive, immediate spike in billable hours. Firms must rapidly reallocate associates to handle the sheer volume of urgent advisory calls, claims reviews, and injunctions to prevent ships from being arrested in foreign ports due to unpaid surge premiums.

Conclusion

Marine insurance underpins global trade by allocating risk across commercial actors and enabling the movement of high-value goods.

At first glance, marine insurance, especially during a crisis can seem like a massive, unfair disadvantage to shipping lines. When underwriters issue sudden 72-hour cancellation notices and demand millions of dollars in “Additional War Risk Premiums” for a single seven-day transit, it often feels more like a financial shakedown than a protective service.

However, looking closely at the mechanics of global trade reveals that the advantages of these policies exponentially outweigh the painful upfront costs. While the premiums are steep, they perform a vital function as:

- they transfer the catastrophic risk of a total hull loss

- shield companies from billion-dollar third-party liabilities (like wreck removals or oil spills)

- satisfy the strict collateral requirements of international banks

Without paying these seemingly disadvantageous premiums, shipowners face instant bankruptcy, and banks freeze the Letters of Credit that fund global commerce. Therefore, marine insurance doesn’t just protect the cargo; it prevents the entire global trade system from grinding to a halt.

Leave a Reply